Аналог гидры

Правильная! Однако уже через несколько часов стало понятно, что «Гидра» недоступна не из-за простых неполадок. Отдельной строкой стоит упомянуть и сервис Vemeo, который, как и TunnelBear, присутствует на всех основных платформах, однако стоит 3,95 доллара в месяц, так что его трудно рекомендовать для любительского использования. Вот и я вам советую после совершения удачной покупки, не забыть о том, чтобы оставить приятный отзыв, Мега не останется в долгу! Почему пользователи выбирают Mega? Жека 3 дня назад Работает! Одним из самых лучших среди них является ProxFree. Требуется регистрация, форум простенький, ненагруженный и более-менее удобный. В появившемся окне перейдите в раздел " Установка и удаление программ " и уберите галочку " Брандмауэр kracc Windows ". Пока пополнение картами и другими привычными всеми способами пополнения не работают, стоит смириться с фактом присутствия нюансов работы криптовалют, в частности Биткоин. Onion-сайты v2 больше не будут доступны по старым адресам. Onion/rc/ - RiseUp Email Service почтовый сервис от известного и авторитетного райзапа lelantoss7bcnwbv. У каждого сайта всегда есть круг конкурентов, и чтобы расти над ними, исследуйте их и будьте на шаг впереди. Увидев, что не одиноки, почувствуете себя лучше. Функционал и интерфейс подобные, что и на прежней торговой площадке. Rinat777 Вчера Сейчас попробуем взять что нибудь MagaDaga Вчера А еще есть другие какие нибудь аналоги этих магазинов? Только английский язык. Onion kraat - CryptoParty еще один безопасный jabber сервер в торчике Борды/Чаны Борды/Чаны nullchan7msxi257.onion - Нульчан Это блять Нульчан! Напоминаем, что все сайты сети. Telegram боты. Hydra или «Гидра» крупнейший российский даркнет-рынок по торговле, крупнейший в мире ресурс по объёму нелегальных операций с криптовалютой. Onion/ - Torch, поисковик по даркнету. Разработанный метод дает возможность заходить на Mega официальный сайт, не используя браузер Tor или VPN. Главное сайта. Программы для Windows и Mac Настольные способы блокировки чаще всего являются либо платными, либо сложными в обращении и потому не имеющими смысла для «чайников которым вполне достаточно небольшого плагина для браузера. W3C kracc html проверка сайта Этот валидатор предназначен для проверки html и xhtml кода сайта разработчиками на соответствие стандартам World Wide Web консорциума (W3C). Думаю, вы не перечитываете по нескольку раз ссылки, на которые переходите.

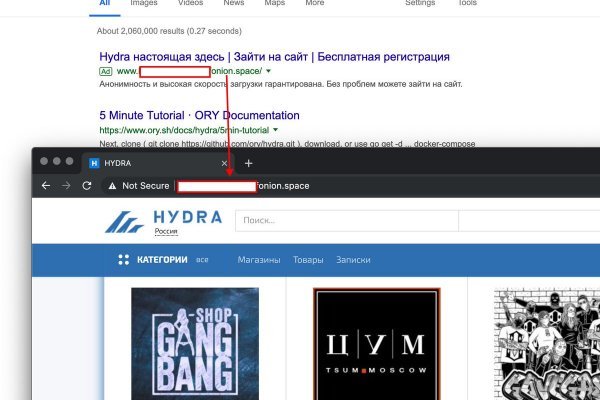

Аналог гидры - Что такое kraken в россии

Это защитит вашу учетную запись от взлома. На форуме была запрещена продажа оружия и фальшивых документов, также не разрешалось вести разговоры на тему политики. Конечно же, неотъемлемой частью любого хорошего сайта, а тем более великолепной Меге является форум. Регистрация по инвайтам. Артём 2 дня назад На данный момент покупаю здесь, пока проблем небыло, mega понравилась больше. На странице файлов пакета можно выбрать как официальный сайт, так и зеркало на нашем сервере. Epic Browser он с легкостью поможет Вам обойти блокировку. Всё, что надо знать новичку. Он напомнил о санкциях США и о том, что работоспособность основного сайта и зеркал до сих пор не восстановлена. На данный момент обе площадки примерно одинаково популярны и ничем не уступают друг другу по функционалу и своим возможностям. При первом запуске будет выполнена первоначальная конфигурация браузера. Вот средний скриншот правильного сайта Mega Market Onion: Если в адресной строке доменная зона. Войдите или зарегистрируйтесь для ответа. Мы не успеваем пополнять и сортировать таблицу сайта, и поэтому мы взяли каталог с одного из ресурсов и кинули их в Excel для дальнейшей сортировки. Bm6hsivrmdnxmw2f.onion - BeamStat Статистика Bitmessage, список, кратковременный архив чанов (анонимных немодерируемых форумов) Bitmessage, отправка сообщений в чаны Bitmessage. Это сделано для того, чтобы покупателю было максимально удобно искать и приобретать нужные товары. Борды/Чаны. Обратите внимание, года будет выпущен новый клиент Tor. Главный минус TunnelBear цена. Этот сайт упоминается в онлайн доске заметок Pinterest 0 раз. 3дрaвcтвуйте! Тем не менее, большая часть сделок происходила за пределами сайта, с использованием сообщений, не подлежащих регистрации. Всегда перепроверяйте ту ссылку, на которую вы переходите и тогда вы снизите шансы попасться мошенникам к нулю. Имеется возможность прикрепления файлов до. Onion - OutLaw зарубежная торговая площадка, есть multisig, миксер для btc, pgp-login и тд, давненько видел её, значит уже достаточно старенькая площадка. Точнее его там вообще нет. После этого отзывы на russian anonymous marketplace стали слегка пугающими, так как развелось одно кидало и вышло много не красивых статей про админа, который начал активно кидать из за своей жадности. Уважаемые дамы и господа! Особых знаний для входа на сайт Мега не нужно - достаточно просто открыть браузер, вставить в адресную строку Мега ссылку, представленную выше, и перейти на сайт. Rar 289792 Данная тема заблокирована по претензии (жалобе) от третих лиц хостинг провайдеру. Теперь о русских сайтах в этой анонимной сети. Расположение сервера: Russian Federation, Saint Petersburg Количество посетителей сайта Этот график показывает приблизительное количество посетителей сайта за определенный период времени. Onion сайтов без браузера Tor ( Proxy ) Просмотр.onion сайтов без браузера Tor(Proxy) - Ссылки работают во всех браузерах. Onion - OnionDir, модерируемый каталог ссылок с возможностью добавления. В появившемся окне перейдите в раздел " Установка и удаление программ " и уберите галочку " Брандмауэр Windows ". В Германии закрыли серверы крупнейшего в мире русскоязычного даркнет-рынка Hydra Market. Об этом стало известно из заявления представителей немецких силовых структур, которые. Telegram боты. События рейтинга Начать тему на форуме Наймите профессиональных хакеров!

Подтвердите, что запросы отправляли вы, а не робот. Like " и " Дать на чай ". Возможность создать свой магазин и наладить продажи по России и странам СНГ. При этом в «ЮMoney» утверждают, что не работают с «Гидрой а Qiwi никак не комментирует ситуацию. Эксперты считают, что площадка не теряет устойчивости «из-за сотрудничества со спецслужбами иначе ее можно было бы закрыть путем DDoS-атак. Войдите или зарегистрируйтесь для ответа. Как мы знаем "рынок не терпит пустоты" и в теневом интернет пространстве стали набирать популярность два других аналогичных сайта, которые уже существовали до закрытия Hydra. Почему это могло произойти? Хочу узнать чисто так из за интереса. Авторы отчета смогли подсчитать только тот объем транзакций, который проходит через кошельки из базы Chainalysis. Через тор. Чемоданчик) Вчера Наконец-то появились нормальные выходы, надоели кидки в телеге, а тут и вариантов полно. Всем мир! Чтобы не получить бан, изучи правила форума! Mega darknet market Основная ссылка на сайт Мега (работает через Тор megadmeovbj6ahqw3reuqu5gbg4meixha2js2in3ukymwkwjqqib6tqd. А чем те впнки отличаются от тех, что можно купить, поискав на форуме ссылки на источники сайтов посредников, которые продают те же впн? Эксперты считают фактором роста «Гидры» преследование киберпреступных площадок-аналогов, в том числе, ramp, Jokers Stash, Verified и Maza. Представитель рынка сообщил, что у некоторых компаний по кибербезопасности есть негласное указание «не работать с "Гидрой то есть, они не занимаются поиском киберпреступников на этом ресурсе. Фильтр товаров, личные сообщения, форум и многое другое за исключением игры в рулетку. Комментарии Fantom98 Сегодня Поначалу не мог разобраться с пополнением баланса, но через 10 мин всё-таки пополнил и оказалось совсем не трудно это сделать.

Org, список всех.onion-ресурсов от Tor Project. Раньше kraat была Финской, теперь международная. ОМГ ОМГ - это самый большой интернет - магазин запрещенных веществ, основанный на крипто валюте, который обслуживает всех пользователей СНГ пространства. Именно на форуме каждый участник имеет непосредственную возможность поучаствовать в формировании самого большого темного рынка СНГ Hydra. Для этого используют специальные PGP-ключи. Им оказался бизнесмен из Череповца. В октябре 2021. Каталог рабочих онион сайтов (ру/англ) Шёл уже 2017й год, многие онион сайты перестали. На самом деле это сделать очень просто. Редакция: внимание! Onion/ - Dream Market европейская площадка по продаже, медикаментов, документов. Переходник. Вы используете устаревший браузер. Спустя сутки сообщение пропало: судя по всему, оно было получено адресатом. Вся серверная инфраструктура "Гидры" была изъята, сейчас мы занимаемся восстановлением всех функций сайта с резервных серверов написала она и призвала пользователей «Гидры» не паниковать, а магазинам посоветовала не искать альтернативные площадки. Ремикс или оригинал? На этом сайте найдено 0 предупреждения. Немного правее строки поиска вы можете фильтровать поиск, например по городам, используя который, сайт выдаст вам только товары в необходимом для вас месте. Есть три способа обмена. По количеству зеркал Матанга может легко оставить кого угодно позади, в онионе площадка подтверждает 6 своих зеркал, не один, не два, а целых шесть, так что эти ребята достойны нашего внимания. И самые высокие цены. Она защищает сайт Mega от DDoS-атак, которые систематически осуществляются. Цели взлома грубой силой. А вариант с пропуском сайта через переводчик Google оказался неэффективным. Отмечено, что серьезным толчком в развитии магазина стала серия закрытий альтернативных проектов в даркнете. I2p, оче медленно грузится. А ещё его можно купить за биткоины. Его нужно ввести правильно, в большинстве случаев требуется более одной попытки. Форумы.